![]() 07/10/2022

07/10/2022

Key Takeaways

Private college loans are an excellent way for prospective students to attend their choice institutions. But how do you get one?

These loans come from all kinds of non-public organizations, such as banks and credit unions. In addition to 100% tuition fee provision, they may also cover payments for books, room & board, and other incidentals.

Looking to get funding for your college education through a private loan? Here’s a detailed guide to get you started!

Like the Federal Pell Grants and the traditional FAFSA process, applying for private college loans requires a systematic approach.

The first step is determining the amount you wish to borrow. Consider the education-related expenses you’re yet to account for here.

The second step is to select the most suitable lender from the numerous options available. Every lender has its unique terms, so intensive research is essential. You’ll have to compare interest rates, repayment flexibility, and unique lender benefits.

Alternatively, you may contact your school for a list of preferred lenders, with more specific eligibility requirements and higher borrowing limits due to the affiliation.

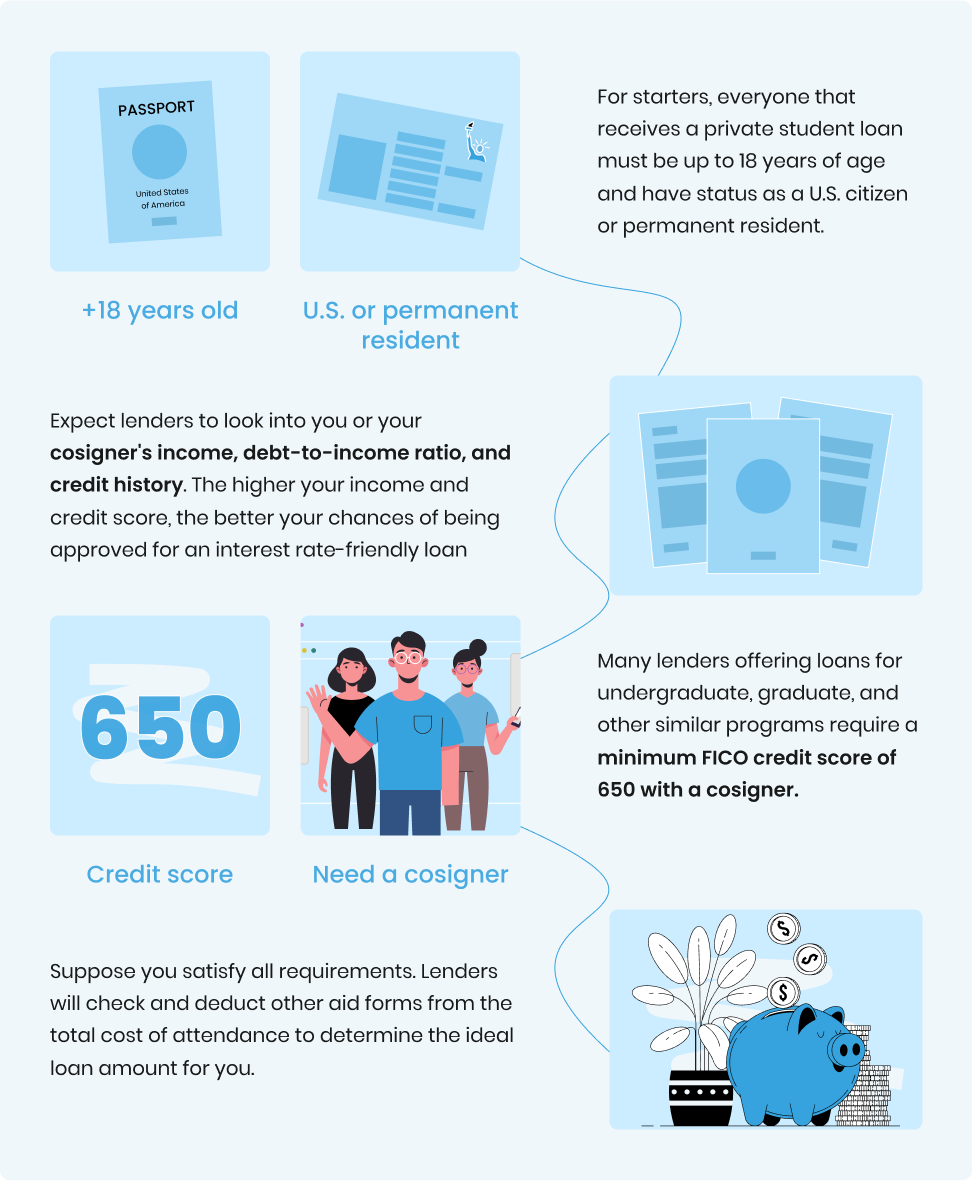

The third step is to identify a cosigner, who acts as a guarantor for your loan agreement. It’s important to note that the cosigner is responsible for repaying your loan if you (the primary borrower) can’t pay it back for whatever reason. Today, the overwhelming majority of undergraduate loans require a cosigner.

You may apply for a private student loan without a cosigner in some instances. However, expect higher interest rates and less favorable repayment terms.

The fourth step is to shortlist all preferred lenders and submit your applications. All private lenders conduct time-consuming hard credit checks to determine eligibility. Therefore, submitting your applications at once may be wiser than waiting for a response from a particular lender before sending out another.

There are many reasons why private college loans may be the right fit. These include higher loan amounts, part-time student eligibility, and strong interest rates.

Also, private loan applications may be strategic, but the process is impressively simple. Unlike a federal application that requires filling out FAFSA, the Free Application for Federal Student Aid, you can complete a private loan application online within minutes.

On the flip side, be aware that private students have a 15 to 20-year cap compared to 30 years for federal student loans. Repayment options are also less agile, with no income-driven repayment options or loan forgiveness/deferment programs.

You should only consider a private student loan if you (or your cosigner) have an excellent credit score and you’ve already maxed out on your subsidized or unsubsidized federal student loan.

Yes, you’ll have to pay back all private college loans. In standard cases, repayment starts six months after graduation with a repayment term of up to 20 years.

If you’re looking for free money, consider public and private need-based or merit-based scholarships offered by public and private organizations.

Each private student loan has its eligibility requirements depending on the issuer. However, there are common grounds.

Finding listings for private college loans is easy. Many online resources are available, including scholarships sites like estgudentloan.com, collegeraptor.com, elmselect.com, and unigo.com.

Many of these sites provide quick, at-a-glance info with essential details for each private student loan, including minimum credit score required, total application time, and fixed/variable APR %. Remember, many lenders will be able to offer a quote with a hard credit check that shouldn’t impact your credit score.

No, your chances are okay, notwithstanding your grant applications. It’s advisable to exhaust all scholarship and grant opportunities before considering college loans, whether federal or private.

There are many differences between a federal loan and a private loan. For starters, federal student loans are distributed by the federal government using the Free Application for Federal Student Aid (FAFSA) application.

The most common types of federal student loans are direct subsidized loans (subsidized Stafford loans), direct unsubsidized loans (unsubsidized Stafford loans), and Perkins loans.

Each loan has different specialties. For example, direct subsidized and Perkins loans require proof of financial need, whereas direct unsubsidized loans don’t. Some also have higher or lower annual, aggregate, or cost of attendance limits than others.

Private student loans are funded by private businesses, such as banks and credit unions, and these options are typically more expensive and are often not subsidized. Additionally, most private student loans require a credit check for yourself and a cosigner, whereas all federal student loans don’t, except for PLUS loans.

All in all, we highly recommend maxing out federal student loan options before applying for private student loans.

Unlike private student loans, all students must complete the FAFSA form. Be sure to adhere to the federal deadline every academic year and stay aware of priority deadlines set by states and colleges.

Accounting for about 2% of all student loans in America, Sallie Mae is one of the largest private lenders in the country. The agency offers student loans for undergraduates, graduates, law schools, nursing school students, and virtually every other field of study.

Other reputable lenders include Credible, LendKey, Ascent, College Ave, and Earnest.

Expect variable rates from 1.13% to 13% and fixed rates from 2.90% to 13%.

For this reason, it’s essential to review all lenders to take advantage of the best rates and terms.

The best private college loans work with your preferred lending requirements. These preferences include interest rate (fixed or variable), loan term length, repayment options, and borrower protections.

Generally, the longer your loan term, the lower your monthly payments. However, this arrangement leads to higher interest rates.

Other private college loans emphasize ease of signing up. Some like the Ascent Independent Student Loan and the Founding U Private Student Loan don’t require a cosigner. Others, like the Ascent Cosigned Student Loan and the MPOWER Private Student loan, cater more to international students.

Lastly, don’t forget instant approval for college loans. Some student loans, such as College Ave Student Loans, come with quick approvals, no origination fees, and completion incentives.

No. Filling out FAFSA is only applicable to federal student loans. These loans include direct subsidized loans (subsidized Stafford loans), direct unsubsidized loans (unsubsidized Stafford loans), and Perkins loans.

Virtually anyone with a good to excellent credit score (600s or greater) can co-sign your loan, including parents, teachers, and friends who are over 18 years of age and are U.S. citizens or permanent U.S. residents. They also have to be gainfully employed without a recent history of bankruptcy.

Sallie Mae is the largest private lender in the country, responsible for close to 2% of all student loans. They lend funds to all types of students, from undergraduates to law school students, offering up to 100% of the total cost of tuition with a possible 20-year repayment period.

Sallie Mae student loans have lots of benefits. For starters, its eligibility criteria are more relaxed than other lenders. Their schemes are available to part-time and foreign-born students, which many other lenders avoid.

Another benefit is complete loan forgiveness if you die or become permanently disabled before full repayment.

A third benefit is its generous conditions for cosigners. All cosigners can be removed from the loan after 12 months of timely payments.

Sallie Mae’s student loans have some drawbacks. For one, there’s a hefty charge for late/returned payment fees. This charge equals 5% of past due payment up to a $25 max along with $20 for returned payments).

Another point of contention is Sallie Mae undergoing a hard credit inquiry to determine interest rates, which may impact your credit score.

How Long Are Co-Signers Responsible for a Loan?

Your co-signer is responsible for your loan throughout its lifetime. However, specific lenders allow you to release your cosigner following 12 months of timely payments. Sallie Mae is one such lender.

What Other Types of Aids Am I Eligible For?

Many financial aid sources are available to set you up upon graduation. These sources include grants, scholarships, work-study jobs, and federal student loans.

Of all, we prefer grants and scholarships. In almost all cases, you don’t have to repay them.

The most popular grants are Pell Grants, Federal Supplemental Educational Opportunity Grants (FSEOG), Iraq and Afghanistan Service Grants, and Teacher Education Assistance for College and Higher Education (TEACH) Grants.

What Is the Federal Work-Study Program?

The Federal Work-Study program helps full and part-time students to pay for college expenses through a part-time job at their college or university. These jobs may be on or off-campus at any organization. Wages are typically at or above the minimum wage.

Your federal work-study award will mandate a total number of work hours based on financial need in terms of hours worked.

Academia Labs has put together this resource for students curious about degrees, schools, and careers available in various scientific fields. We serve as a directory of all institutions students may be interested in joining. Trainees can access the news feed to see popular schools near them as well as other students’ reviews of the schools.

© 2024 AcademiaLabs | All Rights Reserved